Alaska Promissory Note Document

In the picturesque state of Alaska, where the vast landscapes meet the sky, financial transactions between parties often call for a tangible agreement to ensure clarity, legality, and peace of mind for all involved. This is where the Alaska Promissory Note form takes center stage. Serving as a vital financial instrument, this document outlines the specifics of a loan agreement between a borrower and a lender. It meticulously details the amount borrowed, interest rates applicable, repayment schedule, and what should occur if the borrower fails to repay the loan. Designed to be legally binding, this form not only promotes a sense of security but also fosters trust between the parties. It stands as a testament to the importance of documenting financial dealings in a formal manner, enabling both parties to have a clear understanding of their obligations. Ensuring these aspects are meticulously recorded can save a great deal of misunderstanding and legal hassle, making the Alaska Promissory Note form an essential tool in financial transactions across the Last Frontier.

Document Example

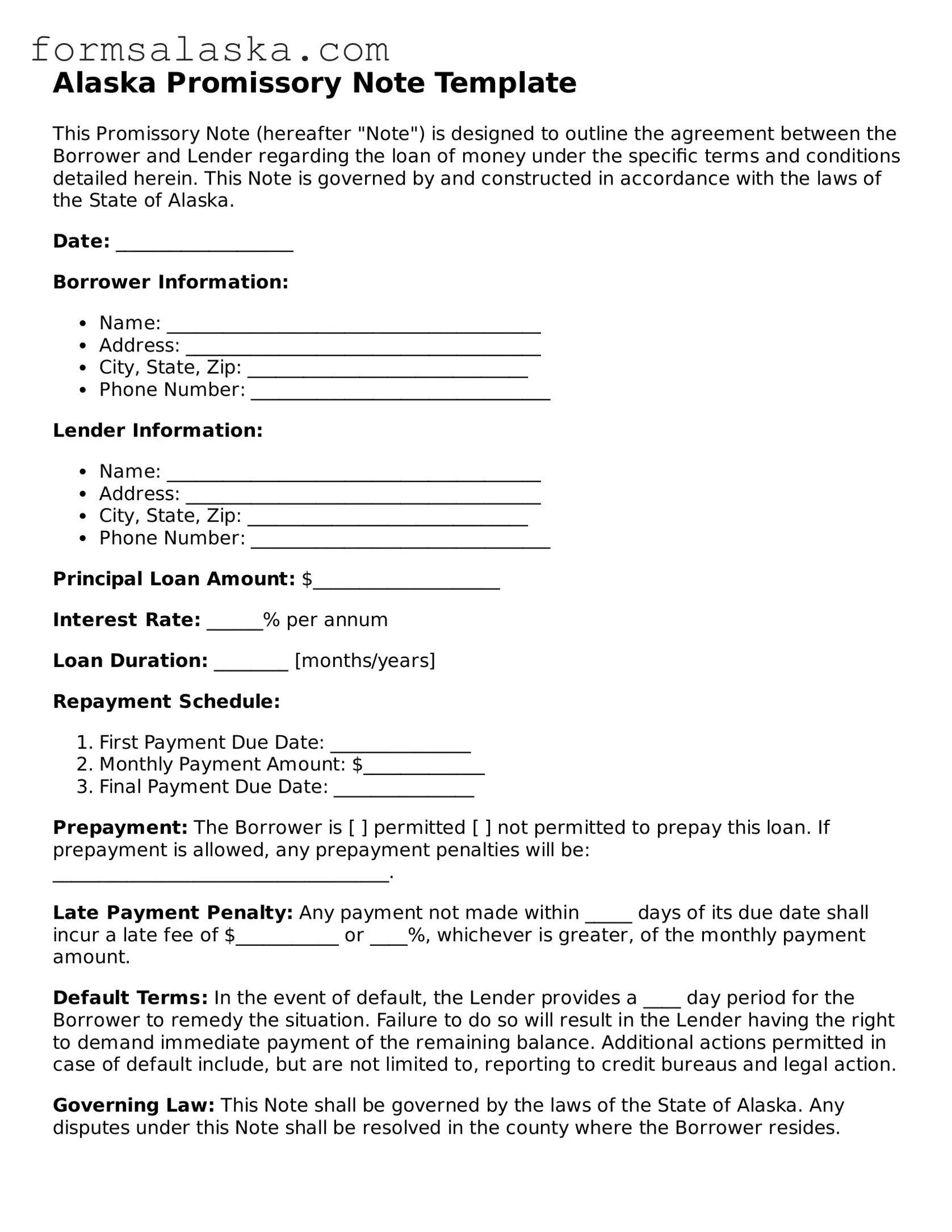

Alaska Promissory Note Template

This Promissory Note (hereafter "Note") is designed to outline the agreement between the Borrower and Lender regarding the loan of money under the specific terms and conditions detailed herein. This Note is governed by and constructed in accordance with the laws of the State of Alaska.

Date: ___________________

Borrower Information:

- Name: ________________________________________

- Address: ______________________________________

- City, State, Zip: ______________________________

- Phone Number: ________________________________

Lender Information:

- Name: ________________________________________

- Address: ______________________________________

- City, State, Zip: ______________________________

- Phone Number: ________________________________

Principal Loan Amount: $____________________

Interest Rate: ______% per annum

Loan Duration: ________ [months/years]

Repayment Schedule:

- First Payment Due Date: _______________

- Monthly Payment Amount: $_____________

- Final Payment Due Date: _______________

Prepayment: The Borrower is [ ] permitted [ ] not permitted to prepay this loan. If prepayment is allowed, any prepayment penalties will be: ____________________________________.

Late Payment Penalty: Any payment not made within _____ days of its due date shall incur a late fee of $___________ or ____%, whichever is greater, of the monthly payment amount.

Default Terms: In the event of default, the Lender provides a ____ day period for the Borrower to remedy the situation. Failure to do so will result in the Lender having the right to demand immediate payment of the remaining balance. Additional actions permitted in case of default include, but are not limited to, reporting to credit bureaus and legal action.

Governing Law: This Note shall be governed by the laws of the State of Alaska. Any disputes under this Note shall be resolved in the county where the Borrower resides.

Amendment: Any amendment to this Note must be in writing and signed by both the Borrower and Lender.

Signatures:

The undersigned have read and agree to the terms of this Note:

Borrower's Signature: ___________________________ Date: _________

Lender's Signature: _____________________________ Date: _________

Document Specs

| Fact | Detail |

|---|---|

| 1. Purpose | Used for documenting a loan between two parties in Alaska. |

| 2. Components | Includes principal amount, interest rate, payment schedule, and maturity date. |

| 3. Type | Can be secured or unsecured, depending on whether collateral is provided. |

| 4. Interest Rate | Must not exceed the legal limit set by Alaska law unless an exemption applies. |

| 5. Governing Law | Governed by Alaska Statutes, including provisions related to interest rates and usury laws. |

| 6. Necessity for Witnesses or Notarization | Not universally required but recommended for legal validation and enforcement. |

| 7. Default Consequences | Specifies the actions the lender can take if the borrower fails to make timely payments. |

| 8. Prepayment | Borrowers may be allowed to pay the loan off early, possibly incurring a prepayment penalty depending on the agreed terms. |

| 9. Amendment Process | Any changes to the note must be in writing and signed by both the lender and the borrower. |

Instructions on How to Fill Out Alaska Promissory Note

Filling out a Promissory Note in Alaska is a critical step towards formalizing a loan agreement between two parties. It serves as a legal document that outlines the borrower's promise to repay the lender as per the agreed terms. This document is beneficial for both parties as it provides a clear and enforceable record of the loan, the repayment schedule, interest rate, and what happens if the borrower fails to make payments. The process requires attention to detail to ensure that all information is accurate and complete, minimizing the chances of future disputes.

To correctly fill out an Alaska Promissory Note form, follow these steps:

- Identify the Parties: Start by writing the full legal names of the lender and the borrower at the top of the form. Specify their relationship and provide contact information, including addresses and phone numbers.

- Specify Loan Amount: Clearly state the principal amount of money being loaned. This should be the amount given to the borrower, excluding any interest.

- Determine the Interest Rate: Agree upon an interest rate for the loan. This should comply with Alaska's usury laws to avoid illegal interest charges. Note the rate annually.

- Set the Repayment Terms: Outline how the borrower intends to repay the loan. This includes the repayment schedule (monthly, quarterly, lump sum, etc.), the start date of payments, and the due date for the loan to be paid in full.

- Include Late Fees: If applicable, specify any late fees for missed payments and after how many days a payment is considered late.

- Address Collateral: If the loan is secured, describe the collateral that the borrower offers as security. Ensure this description is detailed.

- Signatures: Both the lender and the borrower must sign the promissory note. Date the signatures to validate the agreement.

- Witnesses and Notarization: Depending on Alaska's requirements, you may need to have the note witnessed or notarized. This adds an extra layer of authenticity to the document.

Once all sections are completed, review the document carefully. Ensure that both parties understand and agree to all terms listed in the promissory note. This final step is crucial for preventing misunderstandings or legal issues down the line. Once signed and dated, the promissory note becomes a legally binding contract that obligates the borrower to repay the loan as specified. Retain copies for each party's records to maintain a paper trail of the agreement.

What You Should Know About This Form

What is an Alaska Promissory Note form?

An Alaska Promissory Note form is a legal document that outlines a loan's terms between a borrower and a lender in the state of Alaska. It specifies the amount of the loan, the interest rate, repayment schedule, and the obligations of the parties involved. This form is binding and enforceable in the state of Alaska, providing a clear agreement to protect both parties' interests.

How do you legally enforce an Alaska Promissory Note?

To legally enforce an Alaska Promissory Note, it must be signed by both the borrower and the lender, and ideally, it should be notarized. If the borrower fails to meet the agreed repayment terms, the lender can take legal action to recover the loaned amount. This could involve filing a lawsuit in a court of law. The enforceability of the note will depend on its adherence to Alaska state laws, including any statutes related to interest rates and lending practices.

Can modifications be made to a Promissory Note after it has been signed in Alaska?

Yes, modifications can be made to a Promissory Note after it has been signed, but any changes must be agreed upon by both the borrower and the lender. It is highly recommended that any modifications be made in writing and signed by both parties to maintain the document’s legality and enforceability. In some cases, a new promissory note may be created to replace the original agreement.

What happens if a borrower defaults on a Promissory Note in Alaska?

If a borrower defaults on a Promissory Note in Alaska, the lender has the right to pursue various legal remedies to recover the debt. This could include initiating a collection process, seizing collateral if any was pledged against the loan, or filing a lawsuit against the borrower. The specific actions a lender can take will depend on the terms outlined in the promissory note and Alaska state law. It is often advisable for lenders to seek legal counsel to navigate the recovery process effectively.

Common mistakes

When completing the Alaska Promissory Note form, individuals often make mistakes that could potentially impact the legality and enforceability of the agreement. Recognizing and avoiding these common errors can save time, money, and stress in the long run. Below are nine common mistakes people make when filling out this form:

Not specifying the exact amount loaned in clear, unambiguous terms. This detail is crucial for enforcing the terms of the note.

Failure to clearly define the payment schedule, including the due dates and the number of payments. This omission can lead to misunderstandings and disputes.

Omitting the interest rate or not stating it clearly. In Alaska, if an interest rate is not specified, the default rate may be applied, which might not be what the parties intended.

Not including details about collateral, if any is being used to secure the note. This oversight could affect the lender's ability to recover the loaned funds if the borrower defaults.

Leaving out late fees and charges for missed payments. Specifying these terms can incentivize timely repayment and provide compensation to the lender for the inconvenience of delayed payments.

Failing to state the consequences of a default by the borrower. Without this, enforcing the note or taking legal action can become more complicated.

Not having the note signed and dated by all parties involved, including any witnesses or a notary public if required. This formality lends legal weight to the document.

Forgetting to include a clause that clarifies the note may be paid in full before the due date without penalty. This omission might discourage borrowers from settling their debt early.

Ignoring state-specific requirements or clauses that could affect the note's enforceability. It's important to familiarize oneself with Alaska's laws governing promissory notes to ensure the document is compliant.

In drafting a promissory note, it's essential to approach the process with attention to detail and thoroughness. By avoiding these common mistakes, individuals can create a stronger, more enforceable agreement that reflects the true intent of all parties involved.

Documents used along the form

When transactions involve lending or borrowing money, especially in Alaska, the Promissory Note form is a critical document. It formalizes the promise to pay back the borrowed amount under specified conditions. However, this form rarely stands alone. Several other documents are also frequently used in conjunction to ensure the loan arrangement is thorough, complying with legal standards, and protective of all parties involved. Here’s a look at some of those essential documents.

- Loan Agreement: This is a comprehensive contract that details the terms and conditions of the loan. It includes interest rates, repayment schedule, collateral (if any), and what happens in case of default. It’s broader than a promissory note and legally binds both parties.

- Security Agreement: When a loan is secured with collateral, this document outlines the details of that collateral. It ensures the lender has a legal claim to the collateral if the borrower defaults on the loan.

- Guaranty: This document is used when a third party guarantees the loan. It means that if the original borrower fails to repay, the guarantor will cover the debt.

- Amortization Schedule: This illustrates the breakdown of each payment over the course of the loan, showing how much goes towards interest and how much towards reducing the principal amount.

- Mortgage Agreement: In cases where the loan is used to purchase real estate, this document secures the loan with the property being purchased. It gives the lender the right to foreclose on the property if the borrower does not make their loan payments.

- Deed of Trust: Similar to a mortgage agreement but involves a third-party trustee, who holds the title to the property until the loan is paid in full. This is more common in some states than others.

- UCC-1 Financing Statement: For loans involving personal property as collateral (not real estate), this document is filed to publicly declare the lender's interest in the borrower's property.

- Release of Promissory Note: This document is signed by the lender once the loan is fully repaid, releasing the borrower from their obligations under the promissory note.

Together, these documents create a legal framework that safeguards the interests of both borrower and lender. They ensure clarity, enforceability, and peace of mind throughout the lifecycle of the loan. Therefore, when entering into a loan agreement, it’s prudent for both parties to understand not just the Promissory Note but also the role and function of accompanying documents.

Similar forms

A Mortgage Agreement closely resembles an Alaska Promissory Note, as both set the terms for the borrowing and repayment of a sum of money. The key distinction lies in the Mortgage Agreement explicitly using property as security for the debt, ensuring the lender can reclaim the property if the borrower fails to meet the agreed repayment terms. This extra layer of security differentiates it from the more straightforward, unsecured promise to pay found in a promissory note.

Loan Agreements are similar to Alaska Promissory Notes in that they both outline the terms of a loan between a borrower and a lender. However, Loan Agreements are typically more comprehensive, detailing the obligations and rights of each party in greater depth, including clauses on default, governing law, and dispute resolution, which might not be as exhaustively covered in a Promissory Note.

IOU Documents share a purpose with Alaska Promissory Notes by recording an amount owed by one party to another. The primary difference is in their formality and detail; an IOU is often more informal and lacks detailed terms of repayment, interest, and penalties for late payment that a Promissory Note typically includes, making the latter more legally binding.

Debt Settlement Agreements parallel Alaska Promissory Notes in their focus on the repayment of debt but approach the situation from the angle of modifying the original terms of repayment. They come into play when the borrower cannot meet the original terms, and both parties agree on new terms, possibly including a reduction of the total debt, something not typically found in the structure of a promissory note.

Installment Agreements are akin to specific types of Alaska Promissory Notes that set out a repayment plan in installments over a period of time. While both documents establish a schedule for repaying a debt, Installment Agreements are often used for specific types of debt like taxes and might include additional terms related to the specifics of the installment payments, such as penalties for failing to make payments on time.

Personal Guarantee Forms bear similarity to Alaska Promissory Notes to the extent that they both involve commitments to pay. In a Personal Guarantee, however, a third party guarantees to pay the debt of the borrower if they default, adding an extra layer of security for the lender. This contrasts with a Promissory Note’s direct promise from the borrower to the lender.

The Credit Agreement is another document that resembles an Alaska Promissory Note, with both facilitating a loan of some sort. Credit Agreements, however, are generally used for revolving credit situations like credit cards or lines of credit and include complex terms regarding interest rates, credit limits, and repayment terms, offering a broader scope compared to the more focused, typically one-time arrangement detailed in a Promissory Note.

Secured Promissory Notes are a specific variant that shares the basic premise of an Alaska Promissory Note but includes a security interest in the borrower's assets. This security interest provides collateral for the debt, offering the lender protection if the borrower defaults, distinguishing it from unsecured notes that do not provide the lender with claims on the borrower's assets.

Lease Agreements, while distinct in their primary function of granting use or occupation of property, resemble Alaska Promissory Notes in the aspect of structured payments. Instead of repaying a loan, however, the payments in a lease agreement are for the use of the property. Despite this difference, both documents demand regular payments and can include penalties for failing to meet these obligations.

The Bill of Sale document, often used in the sale of personal property, aligns with Alaska Promissory Notes in their essence of establishing an obligation—here, the payment for personal property. While a Bill of Sale cements the terms of a transaction, transferring ownership of items from seller to buyer, a Promissory Note concerns the repayment of money borrowed, showing the broader applicability of structured payment agreements in legal documents.

Dos and Don'ts

Filling out the Alaska Promissory Note form requires attention to detail and a clear understanding of what is being agreed upon between the lender and the borrower. To guide you in this process, here are some dos and don’ts that will help ensure that your promissory note is legally compliant and accurately reflects the terms of the loan.

- Do ensure all parties' full legal names are used on the document. This clarity helps in avoiding any potential disputes over who is obligated to repay the debt.

- Do specify the exact loan amount in U.S. dollars to avoid any confusion about the amount being borrowed.

- Do clearly state the interest rate, making sure it complies with Alaska’s usury laws to prevent the agreement from being considered void or illegal.

- Do detail the repayment schedule, including due dates, to lay out clear expectations for the borrower and protect the lender's investment.

- Don’t leave any sections blank. Incomplete forms may lead to misunderstandings or legal disputes down the line. If a section does not apply, it’s advisable to note that it is not applicable.

- Don’t forget to include the signatures of both the lender and the borrower, as well as the date the note was signed. This is crucial for the document's enforceability.

- Don’t ignore the importance of having a witness or notary public sign the note. Though not always a legal requirement, it can add an extra layer of validity to the agreement.

- Don’t hesitate to seek legal advice if there’s any uncertainty about the terms of the promissory note or its implications. Consulting a professional can save both parties from potential legal headaches in the future.

By following these guidelines, individuals can create a promissory note that is fair, clear, and legally binding. Paying attention to the finer details now can prevent issues from arising in the future, providing peace of mind for both the lender and the borrower.

Misconceptions

When dealing with the Alaska Promissory Note form, several misconceptions can lead to confusion or misunderstandings. Here’s a clarification of some of the common ones:

It's the same as a loan agreement: While both documents relate to borrowing, a promissory note is a promise to pay back a loan under specified terms. A loan agreement typically includes a more detailed outline of the terms and conditions, including the roles and responsibilities of both parties.

Notarization is required: In Alaska, not all promissory notes need to be notarized. Notarization may add a layer of verification, but it's not always a legal requirement for the note to be enforceable.

Only formal businesses can issue them: Individuals can create and issue promissory notes. It's a common misconception that only entities like banks or corporations can issue them.

Interest rates are unregulated: Alaska, like many states, has usury laws that cap interest rates to prevent illegal or excessive interest. Promissory notes must adhere to these limits to remain valid and enforceable.

A signature is all that's needed: While a signature is crucial, a valid promissory note in Alaska should also include details such as the principal amount, interest rate, payment schedule, and what happens in case of a default.

Verbal agreements are just as good: While verbal contracts can be enforceable, a written promissory note is necessary to provide clarity and act as tangible proof of the agreement’s terms.

All promissory notes are secured: Promissory notes can be either secured or unsecured. Secured ones are backed by collateral, while unsecured ones are not, relying solely on the borrower's promise to pay.

They are only for large amounts of money: Promissory notes can be used for loans of any size. They are not limited to large transactions and can be an effective tool for documenting smaller loans as well.

There’s no need to specify the payment schedule: Clearly stating the payment schedule is essential for setting expectations and ensuring there are no misunderstandings about repayment terms.

Only the borrower needs to adhere to the terms: While the borrower must comply with the repayment terms, the lender also has obligations, such as adhering to agreed-upon interest rates and respecting conditions related to early repayment or default.

Key takeaways

When dealing with the Alaska Promissory Note form, it's critical to have a clear understanding of its implications and requirements. This document is a formal agreement between a borrower and a lender, outlining the repayment of a loan. Below are key takeaways to guide you through filling out and using this form:

- Ensure accuracy in all provided information, including the full names and addresses of both the borrower and the lender, to avoid any misunderstandings or legal issues down the line.

- Clearly define the loan amount. This figure should include the principal amount without any ambiguity to ensure both parties are on the same page.

- Specify the interest rate. In Alaska, the interest rate on a promissory note must not exceed the maximum legal rate unless otherwise legally exempt; thus, knowing the current limit is crucial.

- Outline the repayment schedule in detail, including due dates, amounts, and the number of installments. This clarity will help prevent disputes related to payment expectations.

- Understand the consequences of non-payment. The form should specify what actions can be taken if the borrower fails to make timely payments, including late fees and potential legal action.

- Include provisions for early repayment. Some promissory notes allow the borrower to pay off the loan early without penalty, but this must be explicitly stated.

- Joint and several liability should be considered if there are multiple borrowers. This means each borrower is individually responsible for the full amount of the loan.

- Security or collateral might be required for securing the loan. If so, the form should clearly describe what property or asset is being used as security and the conditions under which it could be seized.

- Signatures are essential. Both the borrower and lender must sign the promissory note for it to be legally binding. Witnesses or a notary public may also be required, depending on state law.

- Keep a copy. Both parties should keep a copy of the signed promissory note for their records and future reference.

Understanding these key points ensures that when a promissory note is filled out and used, both the borrower and lender are protected under the law. It's always recommended to consult with a legal professional to address any questions or concerns about the Alaska Promissory Note form or its implications.

Other Popular Alaska Templates

Alaska Will Template - Including personal property distribution lists in your Last Will can prevent conflicts over sentimental items among your heirs.

Incorporate in Alaska - Submission of the Articles of Incorporation is a critical step in protecting personal assets from business liabilities by creating a separate legal entity.

Alaska Power of Attorney - Empowers a designated individual to handle a child's medical emergencies and schooling needs.